cross currency basis chart, central banks’ balance sheet and funding currency

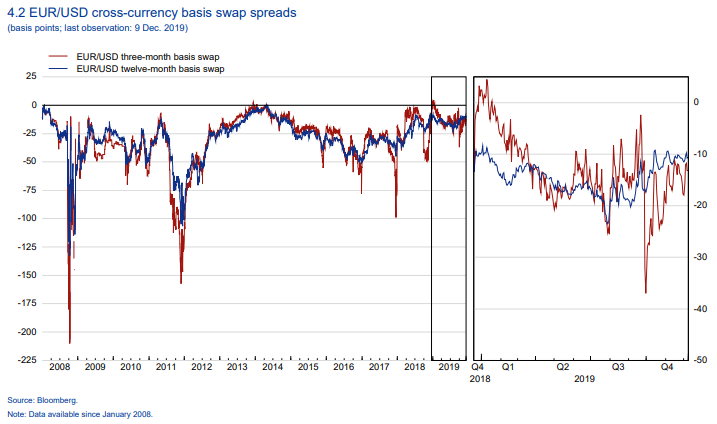

The cross-currency basis, which is the basis spread added mainly to the U.S. dollar London Interbank Offered Rate (USD LIBOR) when the USD is funded via foreign exchange (FX) swaps using the Japanese yen or the euro as a funding currency, has been widening globally since the beginning of 2014. This development is driven by (1) increased demands for U.S. dollars resulting from a divergence in the monetary policy between the U.S. and other advanced countries, (2) global banks’ reduced appetite for market-making and arbitrage due to regulatory reforms, and (3) the decrease in the supply of U.S. dollars from foreign reserve managers/sovereign wealth funds against the background of declines in commodity prices and emerging currency depreciations. (Bank of Japan Review “Recent Trends in Cross-currency Basis“, September 2016)

米連邦準備制度理事会(FRB)が 2013 年に資産購入ペースを「落とす(step down)」可能性を示唆する と、市場の大幅な調整につながった。債券、リスク資産、特にエマージング資産の価格が一斉に下落 し、いわゆる「テーパリング癇癪」が発生した。 (Western Asset " 2013 年の「テーパリング癇癪」からの 4 つの教訓 “)

2013 年の経験を鑑みると、FRB の動き、および市場の反応に向けられる一定の懸念も理解できる。だ が、テーパリング癇癪は、現在の情勢を理解する上で本当に最も重要なのだろうか? この疑問に答える前に、2013 年の経験から得られる以下の 4 つの教訓を念頭に置いておきたい。 1. 市場は 2013 年に FRB の意図(特に短期金利に関する意図)を見誤った。 2. 債券とリスク資産の逆相関は 2013 年も有効であったが、テーパリング癇癪が開始した 1 ヵ 月間は機能しなかった。 3. 縮小開始時における状況は、その後の市場の反応を測る基準として重要である。特定の資産 クラスでは、現在の状況は 2013 年とかなり異なっている(特にエマージング資産のそれは 大幅に異なる)。 4. 現在の環境では、中銀の政策よりも経済成長率やインフレ率の方が債券利回りに及ぼす影 響が大きい。 (Western Asset " 2013 年の「テーパリング癇癪」からの 4 つの教訓 “)

その他:為替のヘッジコスト

https://finance-gfp.com/?p=5804